Ignore at your Own Cost (& Wealth) - Safety First!

- y2jmoneytree

- Nov 25, 2025

- 4 min read

Your ability to handle emergencies determines your ability to build wealth. One unexpected event - a hospital bill, a job cut, a car accident, even a fraud - can force you to dip into savings, redeem investments, and pause SIPs. Compounding doesn’t hate volatility; it hates interruptions.

Priya, a 32-year-old software engineer from Bangalore, was a model investor. For five years, she had diligently put ₹30,000 every month into her mutual fund SIPs, proudly watching her portfolio cross the ₹30 lakh mark. Then, life threw a double curveball. A sudden medical emergency in her family led to a hospital bill of ₹18 lakhs. To make matters worse, the stress caused her to take a 3-month unpaid sabbatical from her job.

Priya had no choice. She first drained her savings, then had to redeem her hard-earned mutual funds to cover the hospital bill and her home loan EMIs. Years of disciplined investing were wiped out. Priya's story is a painful lesson in a simple truth: “safety first” matters.

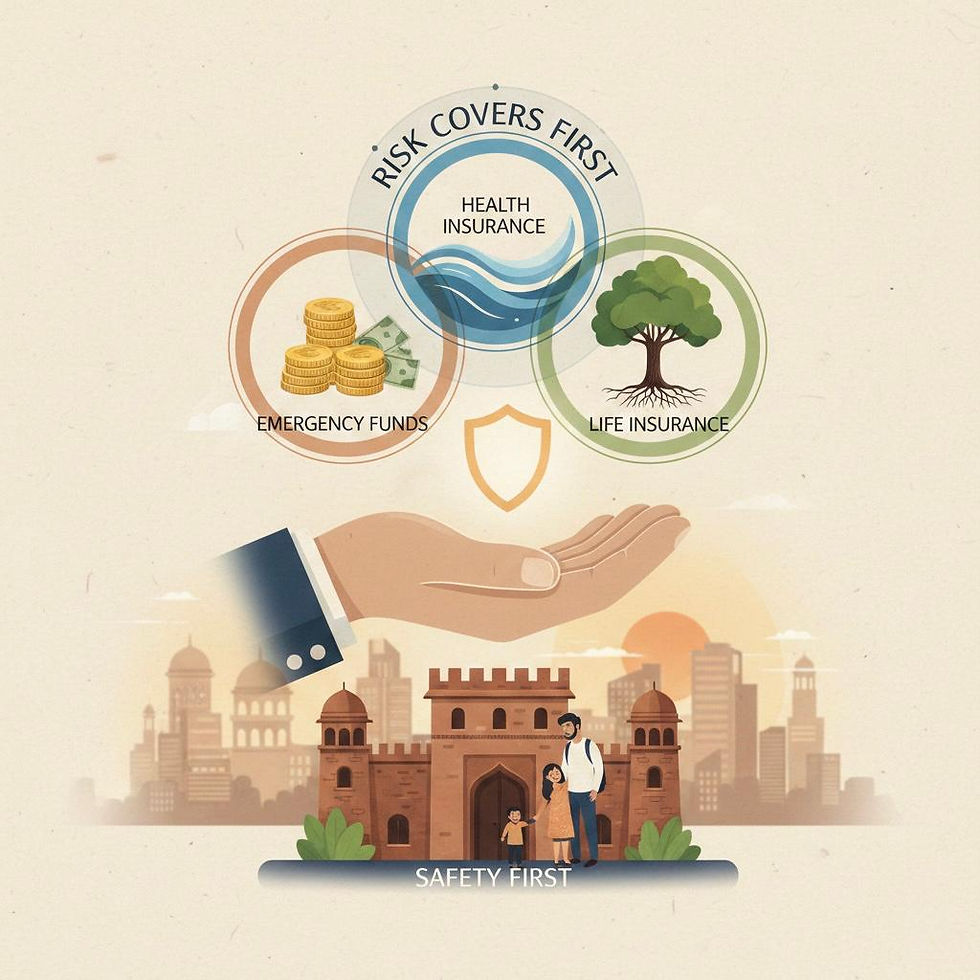

The 6‑Layer Safety Stack

Risk covers are bigger than health and life insurance. They include emergency runway, sinking funds, asset protection, digital hygiene, and documentation. Build this safety stack first, then invest confidently. 3 core layers can be supplemented by additional 3 layers of caution:

Layer 1: The Emergency Fund - Your Financial First-Aid Kit

This is your first line of defense. It's a pool of money set aside exclusively for unexpected life events that disrupt your income or create a sudden expense.

What it covers: Job loss, urgent car/home repairs, an unexpected trip to your hometown for urgent issue. It's for problems that your monthly budget cannot absorb.

How much: A minimum of 6-12 months of your essential living expenses (EMIs, rent, groceries, fees). If you are a freelancer or in an unstable job, aim for 12-18 months.

Where to keep it: This money must be liquid and safe. Do not invest it in stocks or equity funds. Use a separate savings account, a liquid fund, or a sweep-in Fixed Deposit.

Layer 2: Health & Risk Covers – Your Shield Against Catastrophe

Your emergency fund can handle small fires, but what about a raging inferno? A major medical crisis can decimate even a large emergency fund and all your investments. This is where insurance comes in.

Health Insurance: This is your protection against crippling hospital bills. It ensures you get the best medical care without liquidating your assets. Relying only on your office cover is a mistake, as it's temporary and often insufficient.

Personal Accident & Critical Illness Cover: These are supplements. A personal accident policy provides a payout for disability due to an accident, and a critical illness plan gives you a lump sum on diagnosis of major diseases, which can replace lost income during treatment.

Layer 3: Term Life Insurance - The Ultimate Guardian for Your Family

This is the final, most crucial layer of protection if you have financial dependents. It addresses the ultimate risk: the loss of your life and income.

What it does: In your absence, it provides your family with a large, lump-sum amount to pay off any outstanding loans, fund their long-term goals like children's education, and live financially independent lives.

In a relay race, the baton is passed to the next runner to continue the race. A term plan is the financial baton you pass to your family, ensuring they can finish the race to their financial goals, even if you are no longer running with them

Layer 4: Asset Protection (Home, Motor, Travel)

Home: Structure + contents (fire, theft, natural calamities)

Motor: Own‑damage with zero‑depreciation add‑on, engine protect where relevant

Travel: Medical + baggage + trip disruption, especially for international travel

Layer 5: Digital & Cyber Hygiene

Set UPI/card daily limits; enable 2FA; use locked SIM/eSIM and virtual cards for online payments.

Optional cyber insurance add‑ons for identity theft or fraudulent transactions.

Back up documents; avoid sharing OTPs; use secure UPI PINs.

Layer 6: Documentation & Access

Nominees on all accounts/policies, joint holders where appropriate

Will + letter of wishes; consider PoA if needed

DigiLocker for IDs, e‑insurance/e‑cards handy

Consolidate investments via CAMS + KFin statements; store passwords in a secure manager

FAQs

"Why can't my FDs or savings be my emergency fund?"

You can, but it’s not ideal. Savings are often mentally tagged for a goal (like a vacation or a down payment). Using them for an emergency feels like a setback. A dedicated, separate emergency fund creates a clear psychological and financial buffer.

"I have a large emergency fund. Do I still need health insurance?"

Absolutely. A critical illness or major surgery in a good private hospital in India can easily cost ₹15-25 lakhs or more. This can wipe out your entire emergency funds. Health insurance allows you to preserve your emergency fund for what it's meant for.

"Safety Planning seem like a lot of expense before I even start investing."

Think of it as the cost of doing business. The small, predictable cost of insurance premiums and setting aside an emergency fund protects you from a huge, unpredictable loss later. It's the most profitable "expense" you will ever have.

Conclusion

Strong portfolios sit on stronger safety nets. Build your runway, sinking funds, and right‑sized covers, lock your digital doors, and keep critical documents accessible. Then let SIPs and compounding do the heavy lifting. This safety net is like the spare tyre in your car. You hope you never have to use it, but you'd never start a long journey without one.

Happy Investing!

Comments