The Sandwich Generation: Balancing Money From Kids’ Fees To Parents’ Pills

- y2jmoneytree

- Apr 7

- 4 min read

If you’re in your 30s or 40s in India today, this might sound familiar:

School fees, coaching classes and ever-rising education costs for your kids

Medicine bills, health check-ups and sometimes a home nurse for your parents

Your own EMIs, SIPs, taxes, and dreams of a peaceful retirement

Welcome to the sandwich generation – the people squeezed in the middle, supporting both children and ageing parents, often on one or two salaries.

Culturally, Indian families are close-knit. Many of us want to support parents in their later years. At the same time, we want to give our kids better opportunities than we had.

The problem is simple:

One wallet, three generations.

The good news? With thoughtful investment planning in India and some honest conversations, this phase can feel less like a never-ending juggle and more like a clear plan.

Who Is The Sandwich Generation?

Age: late 20s to late 40s.

Stage:

Kids: from preschool to college

Parents: 55–80+, with rising health needs

You: in your main earning years, trying to grow a career or business

You might be:

First-generation urban, maybe first to earn in lakhs

Supporting parents who had little formal retirement planning

Paying home loan EMIs, car loans, and maybe a personal loan

Trying to invest through mutual fund SIP basics, NPS, PPF, etc.

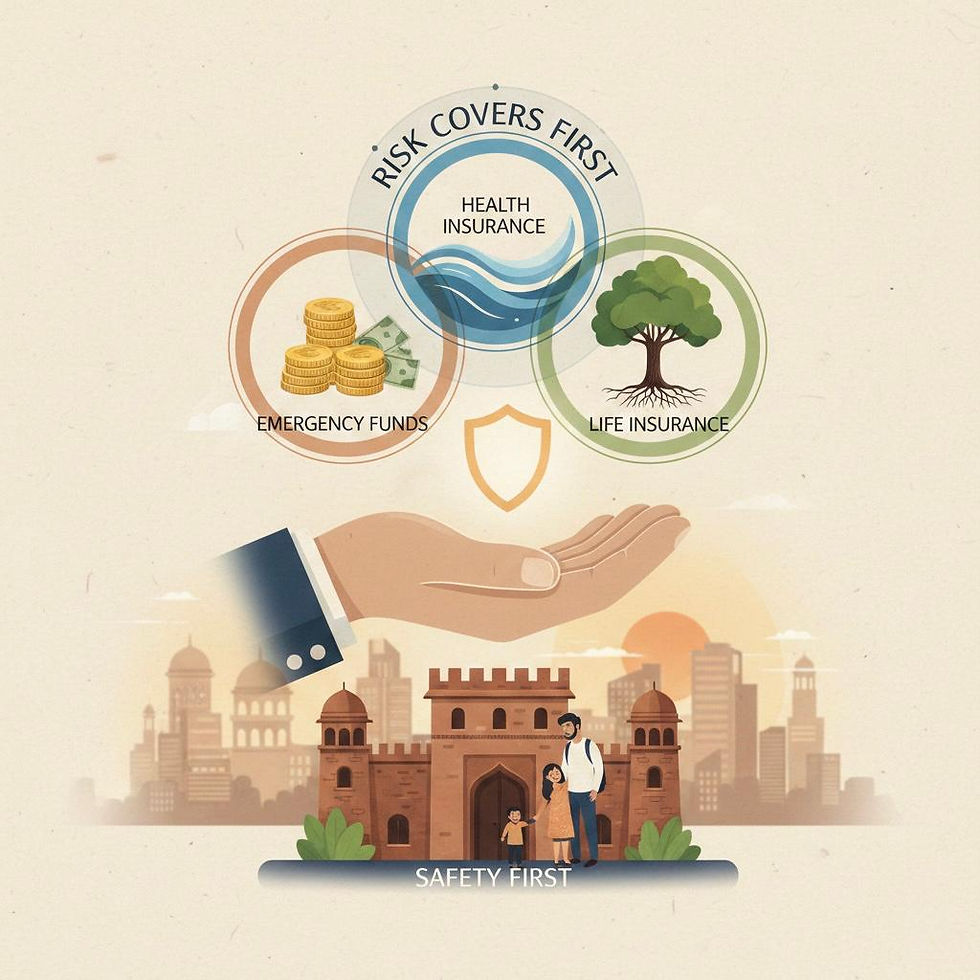

Step 1 – Apply The Oxygen Mask Principle

On flights, they say: “Put on your own oxygen mask before helping others.”It feels selfish. But it’s practical. With money, the “oxygen mask” is:

Emergency Fund

Target at least 6-12 months of household expenses

Keep in savings + liquid or ultra-short-term debt funds

This is your buffer when job/business or health surprises show up

Health Insurance

Adequate cover for:

You, spouse, and kids

Separate cover for parents (often better than mixing in one family floater)

Don’t rely only on corporate health cover; jobs and benefits change

Term Insurance

Pure life cover that replaces your income if you’re not around

Rule of thumb: 10-15 times annual income as a starting point

This protects kids’ education and parents’ basic support if life goes off-script

Without these three, one hospitalisation or job loss can wipe out years of SIPs and push the whole family into debt.

Step 2 – Your three Buckets: Kids, Parents, You

One big mistake is to see all expenses as one big blob. Instead, create three buckets:

1) Kids’ Bucket – Fees Today, Education Tomorrow

Short-term (0–3 years):

School fees, coaching, extracurricular activities

Use: bank account + short-term debt/hybrid funds

Medium-term (5–10 years):

Higher education (engineering, medicine, MBA, foreign studies)

Use:

SIPs in balanced or equity funds (for longer horizons)

Combine with some safe debt for near-goal years

Education inflation in India can be 8-12% per year in many streams.

2) Parents’ Bucket – Health and Dignity

Parents’ needs are less about “goals” and more about uncertainty:

Monthly support: rent, groceries, utilities

Medical: medicines, tests, doctor visits

Big events: surgeries, hospitalisation

Key tools:

Health insurance for parents:

Senior citizen policies can be expensive, but still often better than paying everything from pocket

Disclose pre-existing diseases honestly; waiting periods are standard

Mediclaim + Top-Up:

A base cover (say ₹3-5 lakh)

Plus a super top-up to increase overall protection at lower cost

Super top-up: kicks in after a certain deductible, useful for large bills

When health insurance is in place, you can support parents with time and emotional presence, not just scramble for cash and credit cards every time.

3) Your Bucket – Retirement Is Not Selfish

This is the most ignored part. Many sandwich generation earners say:

“Pehle parents, then kids. Retirement baad mein dekhenge.”

But think ahead: If you don’t build your own retirement corpus, you become financially dependent on your kids later, and the same cycle repeats.

Your bucket should have:

Long-term equity SIPs (diversified equity, index funds, etc.)

NPS/EPF/PPF, depending on your situation

A basic retirement number estimate:

Annual expenses you want in retirement

Multiplied by 20–25 (as a rough starting target)

This is not selfish. This is how you stop the sandwich cycle with you.

Step 3 – Map Cash Flows And Make Trade-Offs Visible

Take one relaxed Sunday, make chai, and open a notebook.

Write down:

Family's monthly income

Fixed costs: EMI, rent, basic living expenses

Kids’ costs: fees, activities, tuition

Parents’ costs: support you give, health expenses

SIPs and investments

You will likely see:

Some lifestyle expenses that can be trimmed (multiple OTT, frequent online orders, frequent upgrading of phones)

Space to increase SIPs a little each year with increments

This is where honest conversations matter.

Step 4 – Talk Openly With Family

In Indian families, money conversations are often emotional. But it doesn't help. Conversations to consider:

What savings, pensions, or assets do parents have?

Do parents already have health insurance?

Parents' preferences for future care (home help, staying with you, etc.)

Shared understanding of priorities: schooling choices, house size, car upgrades

Agreement on supporting both sets of parents fairly within your limits

The goal is not perfect equality, but clarity and fairness.

Conclusion

If you sometimes feel tired, guilty, or behind, remember: You are doing triple duty – for your kids, your parents, and your own future.

The sandwich generation story is not about perfection. It’s about:

Protecting the basics (emergency fund, insurance)

Creating clear buckets for kids, parents and yourself

Making trade-offs consciously, not in panic

Having open conversations instead of silent pressure

A planned approach reduces guesswork and midnight worry.

Happy Investing!

Comments