Click the "Go" Button Now: From Planning to Execution

- y2jmoneytree

- Jan 9

- 3 min read

Ask any professional:

“Do you know you should invest for your future?” – The answer is yes!

“Have you actually mapped all your goals and invested properly for them?” – Usually, not really!

Real life gets in the way:

Office Work

Planning for loan EMIs, School fees, and household stuff

Parents’ care

No time to plan!

So we do what is easiest:

Start one SIP because a friend did, not knowing what/why specific funds

Buy a policy for 80C in February–March (not anymore with the new tax regime!)

Park money in FDs “for safety.”

Maybe some NPS from the office

The result is random, and more confused about whether all this is correct! More than right or wrong, it's randomness at its best!

Our Aim is to turn scattered efforts into a simple 5-step path:

Goal Setting → Risk Covers → Know Your Risk Profile → Asset Allocation → Execution

Step 1 – Goal setting (the blueprint)

You wouldn't board a train without knowing the destination. Why invest without a goal?

You need to move from Vague to SMART:

Vague: "I want to save for my child's education."

SMART: "I need ₹50 Lakhs for my son’s Engineering degree in the year 2032."

The Goal dictates the asset.

1-Pager Blog: http://www.y2jmoneytree.in/post/goals-planning

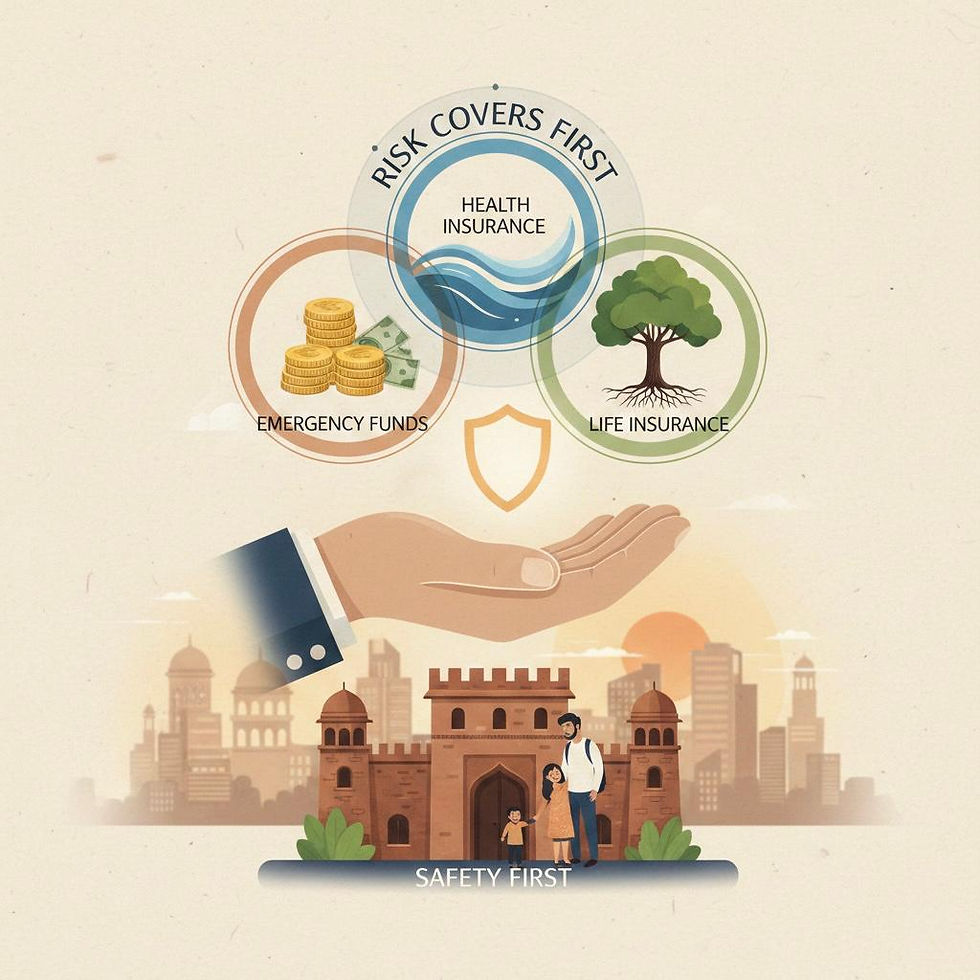

Step 2: Risk Covers (The Foundation)

Before you aim for wealth (Greed), you must secure your life (Fear). If the primary earner passes away or a major illness strikes, your investments will be liquidated instantly to pay bills. Your "House" collapses. Take sufficient coverage for Non-Negotiables: Health Insurance and Life/Term Insurance.

1-Pager Blog: http://www.y2jmoneytree.in/post/risk-cover-first

Step 3: Know Your Money Personality

This is the "Sleep Test." Everyone wants high returns, but not everyone has the stomach for high risk. Your strategy must respect the lower of the two. Be honest with yourself—are you a Test Match player (Conservative) or a T20 hitter (Aggressive)?

1-Pager Blog: http://www.y2jmoneytree.in/post/risk-profile

Step 4: Asset Allocation

This is where the magic happens. A house needs concrete (strength) and glass (beauty). Your portfolio needs a mix of assets to weather different seasons.

Equity: The Engine. Beating inflation over 7+ years

Debt/Bonds: The Anchor. Provides stability when markets crash

Gold/Silver: The Airbag. Usually rises when the economy collapses

1-Pager Blog: http://www.y2jmoneytree.in/post/asset-allocation

Step 5: Execution (The "Go" Button)

This is where 90% of investors fail. They have the plan, they know the products, but they suffer from Analysis Paralysis. They spend months waiting for the "perfect time" or the "best fund." Here is how to bridge the gap between thinking and doing:

1. The "Good Enough" Rule

Don't chase the "Best" fund. The best fund of 2025 will likely not be the best in 2026 or in 2027. Choose a "Good Enough" fund (consistent track record) and start. Time in the market beats timing the market. A decent plan executed today is infinitely better than a perfect plan executed next year.

2. Automate to Remove Willpower

Human beings are terrible at discipline. If you rely on manually transferring money every month, you will find an excuse to spend it. Schedule the Systematic Investment for Salary Date + 2 Days. Invest before you spend.

Execution rule:

“If it’s important, make it automatic. If it’s experimental, keep it manual and small.”

3. The "Top-Up" Ritual

Inflation doesn't stop, so neither should your investment amount.

Strategy: Whenever you get an appraisal or a bonus, divert 50% of that extra income into your investments.

Step-Up SIP: by minimum 5-10% every year. This small habit creates massive wealth over 15 years. E.g. Rs. 10,000 SIP @12% returns gives you Rs. 1 Cr. Whereas, Rs. 10,000 SIP @12% returns and 10% Step-up each year, gives you Rs. 2 Cr. Double the corpus!

4. Review, Don't Stare

Execution also means knowing when not to act.

Wrong: Checking portfolio daily (causes anxiety)

Right: Reviewing portfolio annually (ensures alignment)

Conclusion

One Clear Roadmap Beats 20 Random Investments. Financial Planning is not a one-time event; it is a loop: Goal > Protect > Profile > Allocate > Execute.

Once you execute, you simply review it annually. That’s it. Stop collecting financial products like souvenirs. Start building a portfolio like an architect.

The most important conclusion: Just START it!

Happy Investing!

Comments